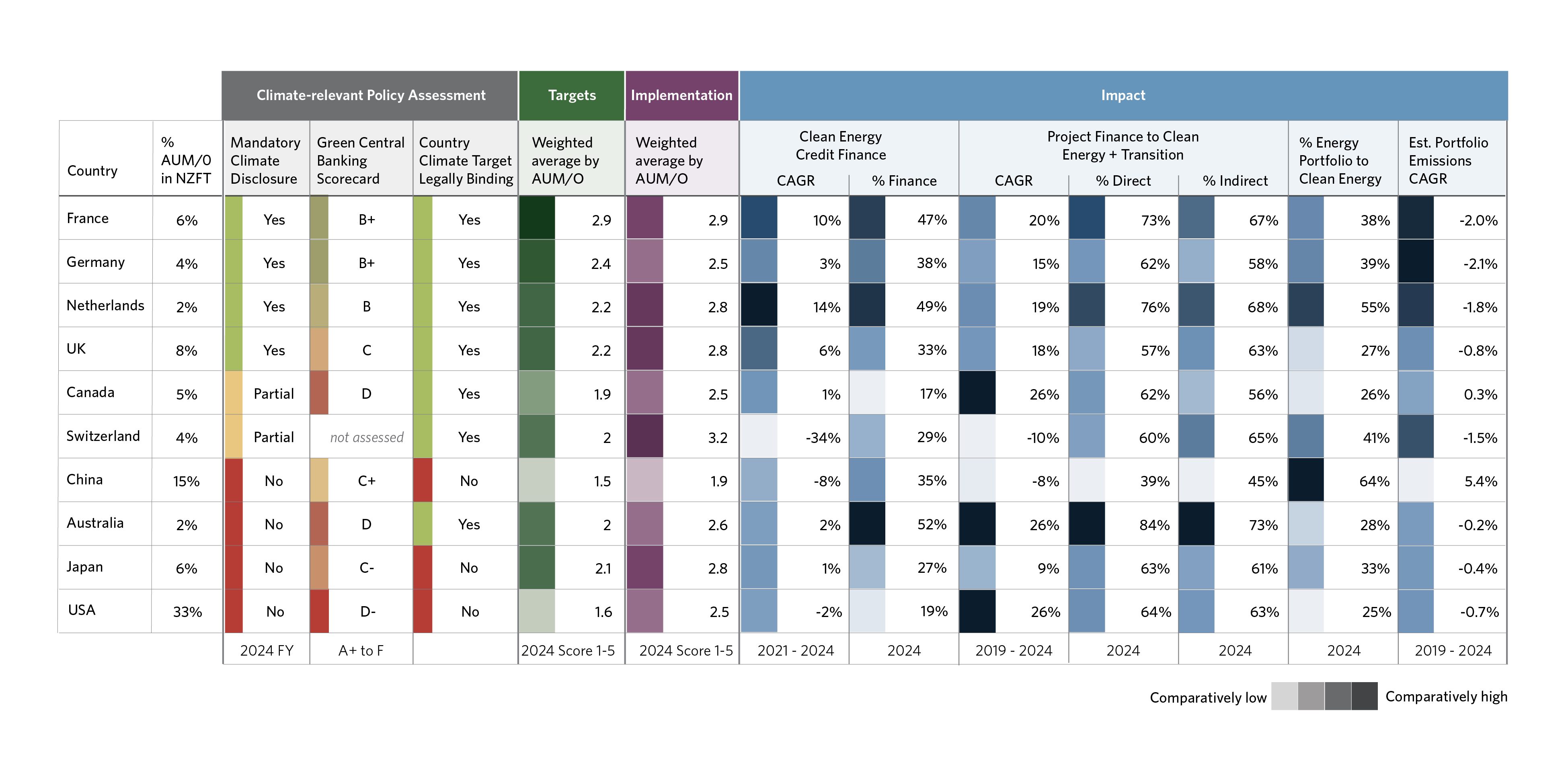

Clean and transition finance is growing, but fossil fuels remain high

Direct finance for clean and transition energy projects reached USD 114 billion in 2024, a 130% increase since 2019. While this represents 65% of the total energy project finance tracked, the remaining 35% going to new fossil fuel projects undermines progress and exacerbates risks. Corporate finance remains even more fossil-heavy: 70% of banks’ new energy finance credit went to fossil fuel activities. In addition, 74% of private financial institutions' energy holdings were in fossil fuels, mostly in companies expanding their operations.